All Categories

Featured

Table of Contents

Indexed universal life policies supply a minimum surefire rate of interest, likewise referred to as a passion attributing floor, which lessens market losses. Claim your cash money worth sheds 8%. Many companies supply a flooring of 0%, suggesting you won't shed 8% of your investment in this situation. Realize that your cash value can decline also with a floor as a result of premiums and other costs.

A IUL is an irreversible life insurance coverage policy that borrows from the residential properties of an universal life insurance plan. Unlike universal life, your cash value expands based on the efficiency of market indexes such as the S&P 500 or Nasdaq.

What makes IUL different from various other policies is that a portion of the premium payment goes right into yearly renewable-term life insurance policy (High cash value Indexed Universal Life). Term life insurance policy, likewise referred to as pure life insurance policy, guarantees survivor benefit settlement. The remainder of the value enters into the total money worth of the policy. Maintain in mind that charges have to be subtracted from the value, which would reduce the cash worth of the IUL insurance coverage.

An IUL plan may be the right selection for a customer if they are looking for a long-lasting insurance coverage product that constructs wide range over the life insurance policy term. This is since it supplies prospective for growth and additionally keeps the a lot of worth in an unstable market. For those who have considerable properties or riches in up-front financial investments, IUL insurance policy will be a terrific wide range management device, especially if someone desires a tax-free retirement.

What is Indexed Universal Life Loan Options?

The rate of return on the policy's money value rises and fall with the index's activity. In contrast to various other plans like variable global life insurance policy, it is much less dangerous. Motivate customers to have a discussion with their insurance representative regarding the ideal choice for their circumstances. When it concerns looking after beneficiaries and taking care of wide range, right here are some of the leading reasons that someone may choose to select an IUL insurance plan: The cash money value that can build up as a result of the interest paid does not count towards revenues.

This indicates a client can use their insurance policy payout as opposed to dipping into their social safety and security cash before they prepare to do so. Each policy should be customized to the client's individual needs, specifically if they are managing substantial possessions. The insurance policy holder and the agent can pick the quantity of risk they consider to be ideal for their requirements.

IUL is a general conveniently adjustable plan for the most part. Because of the rates of interest of universal life insurance policy plans, the price of return that a customer can possibly get is greater than various other insurance coverage. This is due to the fact that the owner and the agent can utilize call options to raise possible returns.

What is the most popular Indexed Universal Life Vs Term Life plan in 2024?

Insurance holders might be drawn in to an IUL policy due to the fact that they do not pay funding gains on the extra cash money worth of the insurance coverage. This can be contrasted to other plans that require taxes be paid on any money that is taken out. This indicates there's a money asset that can be secured at any moment, and the life insurance policy policyholder would certainly not need to stress over paying tax obligations on the withdrawal.

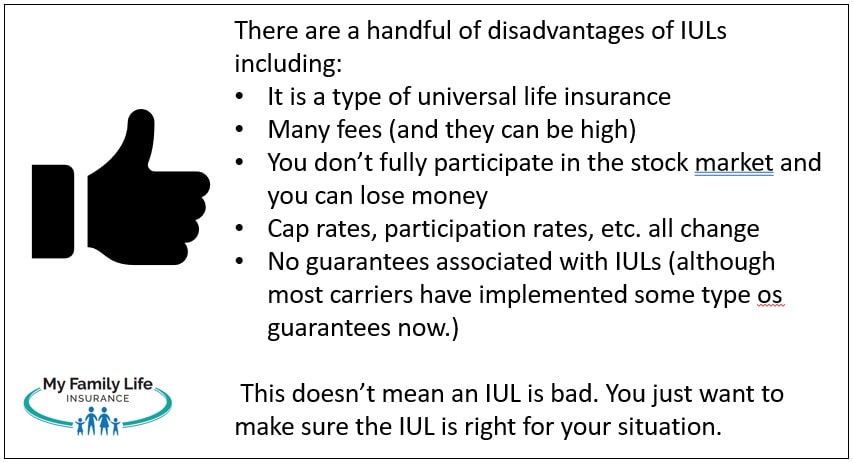

While there are various advantages for a policyholder to select this type of life insurance policy, it's except every person. It is necessary to let the customer recognize both sides of the coin. Right here are a few of the most essential points to encourage a client to take into account prior to opting for this selection: There are caps on the returns a policyholder can get.

The most effective alternative relies on the customer's threat tolerance - Indexed Universal Life cash value. While the fees related to an IUL insurance coverage are worth it for some consumers, it is necessary to be ahead of time with them about the costs. There are superior cost charges and various other administrative fees that can start to build up

No assured passion rateSome other insurance policy policies supply a passion price that is guaranteed. This is not the situation for IUL insurance coverage.

How do I compare Iul Tax Benefits plans?

Consult your tax obligation, legal, or audit specialist regarding your specific circumstance. 3 An Indexed Universal Life (IUL) plan is not thought about a safety and security. Costs and death benefit types are adaptable. It's crediting price is based on the performance of a supply index with a cap rate (i.e. 10%), a flooring (i.e.

8 Irreversible life insurance policy includes two kinds: entire life and global life. Cash money value expands in a getting involved whole life policy with rewards, which are proclaimed every year by the business's board of directors and are not guaranteed. Cash money worth expands in a global life plan with credited interest and reduced insurance policy costs.

Is there a budget-friendly Indexed Universal Life Protection Plan option?

No issue how well you plan for the future, there are occasions in life, both anticipated and unanticipated, that can affect the financial health of you and your loved ones. That's a factor for life insurance policy.

Things like potential tax obligation rises, inflation, monetary emergencies, and planning for occasions like college, retired life, and even wedding celebrations. Some sorts of life insurance policy can assist with these and various other issues too, such as indexed global life insurance policy, or merely IUL. With IUL, your policy can be a funds, since it has the possible to construct value gradually.

You can pick to obtain indexed passion. An index might influence your rate of interest credited, you can not invest or straight participate in an index. Below, your plan tracks, yet is not in fact bought, an outside market index like the S&P 500 Index. This hypothetical example is offered for illustratory purposes just.

Costs and expenditures might reduce plan values. This passion is secured. So if the marketplace decreases, you won't shed any type of interest due to the decline. You can also select to get set interest, one set foreseeable rate of interest month after month, despite the market. Because no solitary allotment will certainly be most efficient in all market environments, your financial specialist can help you figure out which mix may fit your financial goals.

What is the best Indexed Universal Life Retirement Planning option?

That leaves more in your policy to potentially keep growing over time. Down the roadway, you can access any offered cash value via policy loans or withdrawals.

{kind=link}

Latest Posts

What is a simple explanation of Iul Policy?

How long does Iul Plans coverage last?

How do I cancel Iul Growth Strategy?